Delving into the world of Debt Settlement vs Bankruptcy: Full Comparison Guide, readers are invited to explore a detailed analysis that sheds light on the intricacies of these financial decisions.

The following paragraphs will provide a comprehensive breakdown of the key aspects surrounding debt settlement and bankruptcy, offering valuable insights for those navigating these complex choices.

Overview of Debt Settlement and Bankruptcy

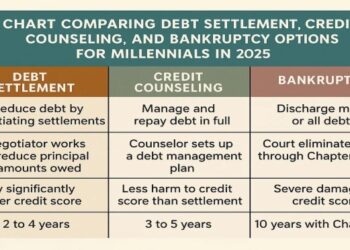

Debt settlement and bankruptcy are two options for individuals facing overwhelming debt. Debt settlement involves negotiating with creditors to settle debts for less than what is owed, typically through a lump sum payment. On the other hand, bankruptcy is a legal process that allows individuals to eliminate or restructure their debts under the protection of the court.

Key Differences Between Debt Settlement and Bankruptcy

- Debt Settlement:

- Allows individuals to negotiate with creditors to reduce the total amount owed.

- Requires making lump sum payments or structured payments to settle debts.

- May have a negative impact on credit score, although less severe than bankruptcy.

- Bankruptcy:

- Provides a legal process to eliminate or restructure debts under court supervision.

- Can result in the discharge of most debts, providing a fresh financial start.

- Has a significant negative impact on credit score and can stay on credit reports for several years.

Examples of Situations Where Each Option May Be More Suitable

- Debt Settlement:

- For individuals with a moderate amount of debt that they can realistically repay with negotiation.

- For those who want to avoid the severe impact of bankruptcy on their credit score.

- Bankruptcy:

- For individuals with overwhelming debt that they cannot repay through other means.

- For those facing imminent threats like foreclosure or wage garnishment.

Process of Debt Settlement vs Bankruptcy

Debt settlement and bankruptcy are two options for individuals struggling with overwhelming debt. Understanding the step-by-step processes of each can help individuals make informed decisions on how to address their financial difficulties.

Debt Settlement Process

Debt settlement involves negotiating with creditors to reduce the amount of debt owed. Here is a general overview of the process:

- Evaluate Debt: Assess the total amount of debt owed and determine which debts are eligible for settlement.

- Save Funds: Start setting aside funds to offer as lump-sum payments to creditors.

- Negotiate with Creditors: Reach out to creditors to negotiate a settlement amount lower than the total debt owed.

- Reach Settlement: Once an agreement is reached, make the agreed-upon payment to the creditor.

- Update Credit Report: Ensure that the settled debt is accurately reflected on your credit report.

Bankruptcy Filing Process

Bankruptcy is a legal process that involves declaring inability to repay debts. Here is an Artikel of the steps involved in filing for bankruptcy:

- Evaluation: Determine if bankruptcy is the best option after considering alternatives.

- Credit Counseling: Complete a credit counseling course from an approved agency within 180 days before filing.

- Filing Petition: Submit a bankruptcy petition to the court, along with financial information and schedules of assets and liabilities.

- Automatic Stay: Upon filing, an automatic stay goes into effect, halting creditor actions like collection calls and lawsuits.

- Meeting of Creditors: Attend a meeting where creditors can ask questions about the bankruptcy case.

- Discharge: If approved, debts may be discharged, meaning creditors can no longer collect on them.

Time Frames and Requirements

Debt settlement and bankruptcy have different time frames and requirements:

| Debt Settlement | Bankruptcy |

|---|---|

| Can take months to years to complete negotiations with creditors. | Chapter 7 bankruptcy typically lasts 3-6 months, while Chapter 13 bankruptcy can last 3-5 years. |

| No specific income or debt requirements, but creditors may prefer larger debts for settlement. | Income limits for Chapter 7 eligibility and debt limits for Chapter 13 repayment plans. |

Impact on Credit Score and Financial Future

When it comes to managing debt through debt settlement or bankruptcy, one crucial aspect to consider is the impact on your credit score and overall financial future. Both options can have long-lasting effects, so it's essential to understand how each choice can influence your financial well-being moving forward.

Debt Settlement and Credit Score

- Debt settlement can negatively impact your credit score since you are essentially paying less than the full amount owed to your creditors. This can result in a lower credit score, making it harder to qualify for loans or credit cards in the future.

- Even though debt settlement can initially lower your credit score, it may be less damaging in the long run compared to bankruptcy, as it shows creditors that you are making an effort to repay your debts.

- It's important to note that the negative impact on your credit score from debt settlement can last for several years, affecting your ability to secure favorable interest rates or financial opportunities.

Long-Term Financial Implications of Bankruptcy

- Choosing bankruptcy can have significant long-term financial implications, as it stays on your credit report for up to ten years. This can make it challenging to qualify for new credit, mortgages, or other financial products.

- Bankruptcy can also affect your ability to secure employment or housing, as some employers and landlords may view a bankruptcy filing as a red flag.

- While bankruptcy provides a fresh start by eliminating most of your debts, it can take time to rebuild your credit and regain financial stability after the process.

Rebuilding Credit After Debt Settlement or Bankruptcy

- After debt settlement, you can start rebuilding your credit by making on-time payments, keeping credit card balances low, and avoiding new debt. Over time, your credit score can gradually improve.

- Following bankruptcy, you can rebuild your credit by applying for a secured credit card, monitoring your credit report for errors, and creating a budget to manage your finances effectively.

- It's essential to be patient and diligent in rebuilding your credit after debt settlement or bankruptcy, as improving your credit score takes time and responsible financial habits.

Legal Ramifications and Protections

When it comes to debt settlement and bankruptcy, there are important legal considerations to keep in mind. Understanding the legal protections offered by each option, as well as the types of debts that can be discharged, is crucial in making an informed decision about your financial future.

Legal Protections in Debt Settlement Agreements

Debt settlement agreements provide legal protections to consumers by negotiating with creditors to reduce the total amount owed. These agreements can help prevent creditors from taking legal action against you, such as filing a lawsuit or garnishing your wages. By working with a reputable debt settlement company, you can benefit from legal safeguards that protect you from aggressive debt collection tactics.

Types of Debts Discharged Through Bankruptcy

Bankruptcy offers the opportunity to discharge certain types of debts, providing a fresh start for individuals overwhelmed by financial obligations. Common types of debts that can be discharged through bankruptcy include credit card debt, medical bills, personal loans, and certain tax debts.

By filing for bankruptcy, you can eliminate these debts and alleviate the burden of repayment.

Potential Legal Consequences and Limitations

While debt settlement can offer legal protections, there are also potential consequences and limitations to consider. For instance, creditors may still pursue legal action if they are not satisfied with the settlement agreement. Additionally, debt settlement can have a negative impact on your credit score and may lead to tax consequences for forgiven debt amounts.On the other hand, bankruptcy is a legal process that can have long-lasting effects on your financial future.

While it can provide relief from overwhelming debt, bankruptcy stays on your credit report for several years and can make it challenging to qualify for new credit or loans in the future. It's important to weigh the legal ramifications and protections of both debt settlement and bankruptcy before making a decision.

Cost Comparison

When considering debt settlement vs bankruptcy, one crucial factor to analyze is the cost associated with each option. Let's break down the expenses involved in debt settlement negotiations and filing for bankruptcy to compare the overall financial impact on the individual.

Debt Settlement Negotiations

- Debt settlement companies typically charge a fee for their services, which can range from 15% to 25% of the total debt amount.

- Additional costs may include upfront fees, monthly maintenance fees, and settlement fees for each debt resolved.

- Individuals may also incur tax consequences on the forgiven debt amount, as the IRS considers it taxable income.

Bankruptcy Filing

- When filing for bankruptcy, individuals must pay court filing fees, which can vary depending on the type of bankruptcy (Chapter 7 or Chapter 13).

- Legal representation fees for a bankruptcy attorney are also common, as navigating the complex legal process requires expertise.

- Bankruptcy may involve selling assets to repay creditors, which can result in additional costs and loss of personal property.

Overall Financial Impact

- Debt settlement may initially seem more cost-effective, but the total expenses can add up, especially with the various fees involved.

- Bankruptcy, while more expensive upfront, offers a fresh start by eliminating most debts and stopping creditor harassment.

- Individuals need to weigh the long-term financial consequences of each option and consider their specific debt situation before making a decision.

Public Record and Privacy Concerns

When it comes to financial decisions like debt settlement and bankruptcy, one crucial aspect to consider is the impact on public record and privacy. Let's delve into how each option affects an individual's financial reputation.

Public Record Implications of Bankruptcy Filings

Bankruptcy filings are a matter of public record, meaning that the details of your bankruptcy case will be accessible to the public. This information can stay on your credit report for up to 10 years, potentially affecting your ability to secure credit or loans in the future.

Privacy Protections in Debt Settlement Agreements

Debt settlement agreements typically do not involve public disclosure of your financial situation. These agreements are private negotiations between you and your creditors, keeping the details of the settlement out of public record. This can offer individuals a level of privacy that bankruptcy filings do not provide.

Impact on an Individual’s Financial Reputation

Opting for bankruptcy may signal to creditors and financial institutions that you have struggled to manage your debts, potentially impacting your financial reputation. On the other hand, debt settlement shows a proactive approach to resolving debts, which may be viewed more favorably by some creditors.

Closing Notes

In conclusion, the comparison between debt settlement and bankruptcy reveals the diverse implications each option carries. As individuals weigh their financial futures, understanding the nuances of these paths becomes crucial in making informed decisions.

FAQ Resource

What are the main differences between debt settlement and bankruptcy?

Debt settlement involves negotiating with creditors to pay off a portion of the debt, while bankruptcy is a legal process that discharges most debts entirely.

How does debt settlement impact credit scores?

Debt settlement can have a negative impact on credit scores, as it involves not paying the full amount owed.

What types of debts can be discharged through bankruptcy?

Most unsecured debts like credit card debt, medical bills, and personal loans can be discharged through bankruptcy.

![Average Corporate Lawyer Salary [2024] | Things to Know | Finbold](https://legal.gamevibes.life/wp-content/uploads/2026/05/Screenshot-2023-12-18-at-13.48.56-1024x630-1-120x86.jpg)

{kind=link}